Form 656 Booklet

Offer in

Compromise

CONTENTS

■ What you need to know ................................................................................ 1

■ Paying for your offer .................................................................................... 3

■ How to apply ................................................................................................ 4

■ Completing the application package ............................................................ 5

■ Important information ................................................................................... 6

■ Removable Forms - Form 433-A (OIC), Collection Information Statement

for Wage Earners and Self-Employed Individuals; Form 433-B (OIC),

Collection Information Statement for Businesses; Form 656, Offer in

Compromise ................................................................................................ 7

■ Application Checklist .....................................................................................29

IRS contact information

If you want to see if you qualify for an offer in compromise before filling out the paperwork, you may use

the Offer in Compromise (OIC) Pre-Qualifier tool. The questionnaire format assists in gathering the

information needed and provides instant feedback as to your eligibility based on the information you

provided. The tool will also assist you in determining a preliminary offer amount for consideration of an

acceptable offer but is not a guarantee of acceptance. Access the tool at IRS.gov/OICtool or by

scanning the QR code with your smart device.

All taxpayers have a set of fundamental rights they should be aware of when interacting with the IRS.

Explore your rights and our obligations to protect them. For more information on your rights as a

taxpayer, go to IRS.gov/Taxpayer -Bill-of-Rights.

If you have questions regarding qualifications for an offer in compromise, please call our toll-free number at

800-829-1040. A video on how to complete an offer in compromise is available for viewing on our website at

https://www.irsvideos.gov/Individual/PayingTaxes/CompletingForm656-OfferInCompromiseApplication. Forms

and publications are available by calling 800-TAX-FORM (800-829-3676), by visiting your local IRS office, or at

IRS.gov. For answers to frequently asked questions about the offer process from submission to closure see

Offer in Compromise FAQs.

Taxpayer resources

The Taxpayer Advocate Service (TAS) is an independent organization within the Internal Revenue Service (IRS)

that helps taxpayers and protects taxpayers' rights. TAS can offer you help if your tax problem is causing a financial

difficulty, you’ve tried and been unable to resolve your issue with the IRS, or you believe an IRS system, process, or

procedure just isn't working as it should. If you qualify for TAS assistance, which is always free, TAS will do

everything possible to help you. Visit www.taxpayeradvocate.irs.gov or call 877-777-4778.

Low Income Taxpayer Clinics (LITCs) are independent from the IRS and TAS. LITCs represent individuals whose

income is below a certain level and who need to resolve tax problems with the IRS. LITCs can represent taxpayers in

audits, appeals, and tax collection disputes before the IRS and in court. In addition, LITCs can provide information

about taxpayer rights and responsibilities in different languages for individuals who speak English as a second

language. Services are offered for free or a small fee. For more information or to find an LITC near you, see the LITC

page at www.taxpayeradvocate.irs.gov/litc or IRS Publication 4134, Low Income Taxpayer Clinic List. This publication

is also available online at IRS.gov/forms-pubs or by calling the IRS toll-free at 800-TAX-FORM (800-829-3676).

WHAT YOU NEED TO KNOW

What is an Offer? An Offer in Compromise (offer) is an agreement between you (the taxpayer) and

the IRS that settles a tax debt for less than the full amount owed. The offer

program provides eligible taxpayers an opportunity to resolve their tax debt. The

ultimate goal is a compromise that suits the best interest of both the taxpayer and

the IRS. Generally, you must make an appropriate offer based on what the IRS

considers your ability to pay.

Submitting an application does not ensure that the IRS will accept your offer.

It begins a process of evaluation and verification by the IRS, taking into

consideration any special circumstances that may affect your ability to pay.

Are You Eligible? Before your offer can be considered, you must (1) file all tax returns you are legally

required to file, (2) have received a bill for at least one tax debt included on your

offer, (3) make all required estimated tax payments for the current year, and (4) if

you are a business owner with employees, make all required federal tax deposits

for the current quarter and the two preceding quarters.

Note: If it is determined you have not filed all tax returns you are legally

required to file, the IRS will apply any initial payment you sent with your offer

to your tax debt and return both your offer and application fee to you. You

cannot appeal this decision.

Bankruptcy, Open Audit, Innocent

Spouse Claim, or Deactivated ITIN

If you or your business is currently in an open bankruptcy proceeding, you are not

eligible to apply for an offer. Any resolution of your outstanding tax debts generally

must take place within the context of your bankruptcy proceeding.

Resolve any open audit or outstanding innocent spouse claim issues before

submitting an offer.

We will not consider an offer with a deactivated ITIN. If you have a deactivated

ITIN, please complete the Form W-7, Application for IRS Individual Taxpayer

Identification Number, and have it reactivated. Once completed, you may submit

an Offer in Compromise.

Can You Pay in Full? Generally, the IRS will not accept an offer if you can pay your tax debt in full

through an installment agreement or equity in assets.

Note: Adjustments or exclusions, which may be considered during the offer

investigation, such as allowance of $1,000 to a bank balance or $3,450 against the

value of a car, are only applied if you are an individual and after we determine you

cannot full pay the liabilities from equity in assets, an installment agreement, or a

combination of both.

Your Tax Refunds The IRS may keep any tax period refund, including interest, processed through the

date the IRS accepts your offer by offsetting it against your tax debt, as applicable.

For example, the IRS accepts your offer on July 1, 2022, and you file your 2021

Form 1040 on April 15, 2022, showing a refund; the IRS will apply that refund to

your outstanding tax debt. Since your tax refund may be offset to the tax liability

while the offer is pending, assistance from Taxpayer Advocate or the IRS at

800-829-1040 could be available for taxpayers (other than businesses) facing

economic hardship. The refund is not considered as a payment toward your

offer.

Doubt as to Liability If you have a legitimate doubt that you owe part or all of the tax debt, complete and

submit a Form 656-L, Offer in Compromise (Doubt as to Liability). To request a

Form 656-L, visit IRS.gov or a local IRS office or call toll-free 800-TAX-FORM

(800-829-3676).

Note: Do not submit both an offer under Doubt as to Liability and an offer

under Doubt as to Collectibility or Effective Tax Administration at the same

time. You must resolve any doubt you owe part or all of the tax debt before

submitting an offer based on your ability to pay.

1

Notice of Federal Tax Lien A lien is a legal claim against all your current and future property. When you don’t

pay your first bill for taxes due, a lien is created by law and attaches to your

property. A Notice of Federal Tax Lien (NFTL) provides public notice to creditors.

The IRS files the NFTL to establish priority of the IRS claim versus the claims of

certain other creditors. The IRS may file a NFTL at any time. You may be entitled

to file an appeal under the Collection Appeals Program (CAP) before this occurs or

request a Collection Due Process hearing after this occurs. The IRS may be

entitled to any proceeds from the sale of property subject to the lien(s). If you sell

the property prior to the release of the lien, excess property sale proceeds may be

applied to your tax liability, even if your offer has been accepted.

Trust Fund Taxes If your business owes liabilities that include trust fund taxes, the IRS may hold

responsible individuals liable for the trust fund portion of the tax pursuant to

applicable law. Trust fund taxes are the money withheld from an employee's

wages, such as income tax, Social Security, and Medicare taxes. If the IRS

accepts an offer from an employer for a portion of the trust fund tax liability, the

remainder of the trust fund taxes may be collected from the responsible parties.

You are not eligible for consideration of an offer unless the trust fund portion of the

tax is paid, or the IRS has made the Trust Fund Recovery Penalty determination(s)

on all potentially responsible individual(s). However, if you are submitting the offer

as a victim of payroll service provider fraud or failure, the Trust Fund Recovery

Penalty assessment discussed above is not required prior to submitting the offer.

Other Important Facts You have the right to appeal an offer rejection, but not the return of an offer.

Penalties and interest will continue to accrue while your offer is considered by the

IRS.

After you submit your offer, you must continue to timely file and pay all required tax

returns, estimated tax payments, and federal tax payments for yourself and any

business in which you have an interest. Failure to meet your filing and payment

responsibilities during consideration of your offer will result in the IRS

returning your offer. If the IRS accepts your offer, you must continue to stay

current with all tax filing and payment obligations through the fifth year after your

offer is accepted.

Note: If you have filed your tax returns but you have not received a bill for at least

one tax debt included on your offer, your offer and application fee may be returned

and any initial payment sent with your offer will be applied to your tax debt. To

prevent the return of your offer, wait until you have received a bill for at least

one tax debt and then include a copy of any tax return filed within 12 weeks

of this offer submission.

We can't process your offer if the IRS referred your case involving all tax periods

and liabilities identified in the offer to the Department of Justice. In addition, we

cannot compromise any tax liability arising from a restitution amount ordered by a

court or a tax debt reduced to judgment. Furthermore, we will not compromise any

IRC § 965 tax liability for which an election was made under IRC § 965(i). You

cannot appeal this decision.

The law requires the IRS to make certain information from accepted offers

available for public inspection and review. Find instructions to request a public

inspection file at IRS.gov keyword "OIC".

The IRS may levy your assets up to the time the IRS official signs and

acknowledges your offer as pending. In addition, the IRS may keep any proceeds

received from the levy. If your assets are levied after your offer is submitted and

pending evaluation, immediately contact the IRS at the phone number listed on the

levy.

If you currently have an approved installment agreement, you will not be required

to make your installment agreement payments while we consider your offer. If your

offer is not accepted and you have not incurred any additional tax debt, the IRS will

reinstate your installment agreement.

2

PAYING FOR YOUR OFFER

Application Fee Offers require a $205 application fee.

Exception: If you are an individual and meet the Low-Income Certification

guidelines, there is no requirement to submit any offer payments or the

application fee upon submission or during the consideration of your offer.

You are considered an individual if you are seeking compromise of a liability for

which you are personally responsible, including any liability you incurred as a sole

proprietor.

Payment Options You must select a payment option and include the initial payment with your offer.

The amount of the initial payment and subsequent payments will depend on the

total amount of your offer and which of the following payment options you choose:

Lump Sum: This option requires 20% of the total offer amount to be paid with the

offer and the remaining balance paid in 5 or fewer payments within 5 or fewer

months of the date your offer is accepted.

Periodic Payment: This option requires you to make the first payment with the

offer and the remaining balance paid in monthly payments within 6 to 24 months,

in accordance with your proposed offer terms.

Note: Under the periodic payment option, you must continue to make

monthly payments while the IRS is evaluating your offer. If you fail to make

these payments at any time prior to receiving a final decision letter, the IRS may

return your offer. You cannot appeal this decision. Total payments must equal the

total offer amount. Generally, payments made on an offer will not be returned.

The initial payment and monthly payments are not required if you meet the Low-

Income Certification guidelines. If you qualified under the Low-Income Certification

and are not required to submit payments while the offer is under consideration,

your first payment will be due 30 calendar days after acceptance of the offer,

unless another date is agreed to in an amended offer.

If you do not have sufficient cash to pay for your offer, you may need to consider

borrowing money from a bank, friends, and/or family. Other options may include

borrowing against or selling other assets.

If you are an individual, use the OIC Pre-Qualifier tool at IRS.gov/OICtool to

assist in determining a starting point for your offer amount.

Note: You may not pay your offer amount with an expected or current tax

refund, money already paid, funds attached by any collection action, or

anticipated benefits from a capital or net operating loss. If you are planning to

use your retirement savings from an IRA or 401k plan, you may have future tax

debt as a result. Contact the IRS or your tax advisor before taking this action.

3

HOW TO APPLY

Application Process The application must include:

• Form 656, Offer in Compromise

• Completed and signed Form 433-A (OIC), Collection Information Statement for

Wage Earners and Self-Employed Individuals, if applicable

• Completed and signed Form 433-B (OIC), Collection Information Statement for

Businesses, if applicable

• $205 application fee, unless you meet Low-Income Certification Guidelines

• Initial offer payment based on the payment option you choose, unless you

meet Low-Income Certification Guidelines

Note: Your offer(s) cannot be considered without the completed and signed

Form(s) 656, 433-A (OIC), 433-B (OIC) (if applicable), and supporting

documentation.

If You and Your Spouse Owe

Joint and Separate Tax Debts

If you and your spouse have joint tax debt(s) and you or your spouse are also

responsible for separate tax debt(s) (including Trust Fund Recovery Penalty),

you will each need to send in a separate Form 656. You will complete one Form

656 for yourself listing all your joint and any separate tax debt(s) and your

spouse will complete one Form 656 listing all their joint and any separate tax

debt(s), for a total of two Forms 656.

If you and your spouse or ex-spouse have a joint tax debt and your spouse or ex-

spouse does not want to be part of the offer, you may submit a Form 656 to

compromise your responsibility for the joint tax debt.

Each Form 656 will require the $205 application fee and initial payment

unless you are an individual and meet the Low-Income Certification

guidelines.

If You Owe Individual and

Business Tax Debt

If you have individual and business tax debt that you wish to compromise, you will

need to send in two Forms 656. Complete one Form 656 for your individual tax

debt(s) and one Form 656 for your business tax debt(s). Each Form 656 will

require the $205 application fee and initial payment.

Note: A business is defined as a corporation, partnership, or any business that is

operated as other than a sole-proprietorship. You may not compromise an

individual's share of a partnership debt. The partnership must submit its own offer

based on the partnership's and partners' ability to pay.

4

COMPLETING THE APPLICATION PACKAGE

To calculate an offer amount, you will need to gather information about your

financial situation, including cash, investments, available credit, assets, income,

and debt.

You will also need to gather information about your household's average gross

monthly income and expenses. The household includes all those in addition to

yourself who contribute money to pay expenses relating to the household such as:

rent, utilities, insurance, groceries, etc. This is necessary for the IRS to accurately

evaluate your offer. The IRS may also use this to determine your share of the total

household income and expenses.

In general, the IRS will not consider expenses for tuition for private schools,

college expenses, charitable contributions, and other unsecured debt payments as

part of the expense calculation.

Step 1 – Gather Your Information

Step 2 – Fill out Form 433-A

(OIC), Collection Information

Statement for Wage Earners and

Self-Employed Individuals

Fill out Form 433-A (OIC) if you are an individual wage earner, operate or operated

as a sole proprietor, or are authorized to submit an offer on behalf of the estate of

a deceased individual. If you are married but living separately from your spouse

then you each must submit a Form 433-A (OIC). If the IRS requests information

that is not provided by a spouse, then the IRS may choose to return the offer. This

will assist in the calculation of an appropriate offer amount based on your assets,

income, expenses, and future earning potential. You will have the opportunity to

provide a written explanation of any special circumstances that affect your financial

situation.

Step 3 – Fill out Form 433-B (OIC),

Collection Information Statement

for Businesses

Fill out Form 433-B (OIC) if the business is a Corporation, Partnership, or LLC.

This will assist in the calculation of an appropriate offer amount based on the

business assets, income, expenses, and future earning potential. If the business

has assets used to produce income (for example, a tow truck used in the business

for towing vehicles), the business may be allowed to exclude equity in these

assets.

Step 4 – Attach Required

Documentation

You will need to attach supporting documentation with Form(s) 433-A (OIC) and

433-B (OIC). See a list of the documents required at the end of each form. Include

copies of all required attachments. Do not send original documents.

Step 5 – Fill out Form 656, Offer

in Compromise

Fill out Form 656. The Form 656 identifies the tax years and type of tax you would

like to compromise. It also identifies your offer amount and the payment terms.

Your offer amount must be equal to or greater than the amount calculated in Form

433-A(OIC) or 433-B(OIC).

Step 6 – Include Initial Payment

and $205 Application Fee

Include a personal check, cashier's check, or money order for your initial payment

based on the payment option you selected (20% of the offer amount for a lump

sum offer or the first month's payment for a periodic payment offer). Generally,

initial payments will not be returned but will be applied to your tax debt if your offer

is not accepted.

If you choose to pay the fee and offer payment by personal check, cashier’s

check, or money order, provide a separate personal check, cashier’s check,

or money order for each fee and offer payment you submit. Make checks or

money orders in U.S. dollars and payable to the "United States Treasury." As

an alternative to checks or money orders, you may pay the fee and offer payment

electronically through the Electronic Federal Tax Payment System.

Reminder: If you meet the Low-Income Certification guidelines DO NOT send

any money.

Step 7 – Mail the Application

Package

Make a copy of your application package and keep it for your records.

Mail the completed application package to the appropriate IRS facility. See page

29, Application Checklist, for details.

Note: If you are working with an IRS employee, let them know you are

sending or have sent an offer to compromise your tax debt(s).

5

IMPORTANT INFORMATION

After You Mail Your Application: We will contact you after we receive and review your offer application. Promptly

reply to any requests for additional information within the time frame specified.

Failure to reply timely will result in the return of your offer without appeal rights.

If we accept your offer, you must continue to timely file all required tax returns and

timely pay all estimated tax payments and federal tax payments that become due

in the future. If you fail to timely file and timely pay any tax obligations that become

due within the five years after your offer acceptance we may default your offer. If

we default your offer, you will be liable for the original tax debt, less payments

made, and all accrued interest and penalties. An offer does not stop the accrual of

interest and penalties. Please note that if your final payment is more than the

agreed amount, we will not return the money but will apply it to your tax debt.

In addition, we may default your offer if you fail to promptly pay any tax debts

assessed after acceptance of your offer for any tax years prior to acceptance that

were not included in your original offer.

6

Catalog Number 55896Q www.irs.gov

Form

433-A (OIC) (Rev. 4-2024)

Form 433-A (OIC)

(April 2024)

Department of the Treasury — Internal Revenue Service

Collection Information Statement for Wage Earners and

Self-Employed Individuals

Use this form if you are

● An individual who owes income tax on a Form 1040, U.S.

Individual Income Tax Return

● An individual with a personal liability for Excise Tax

●

An individual responsible for a Trust Fund Recovery Penalty

● An individual who is self-employed or has self-employment

income. You are considered to be self-employed if you are in

business for yourself, or carry on a trade or business.

● An individual who is personally responsible for a partnership

liability (only if the partnership is submitting an offer)

● An individual who is submitting an offer on behalf of the

estate of a deceased person

Note: Include attachments if additional space is needed to respond completely to any question. This form should only be used with the Form

656, Offer in Compromise.

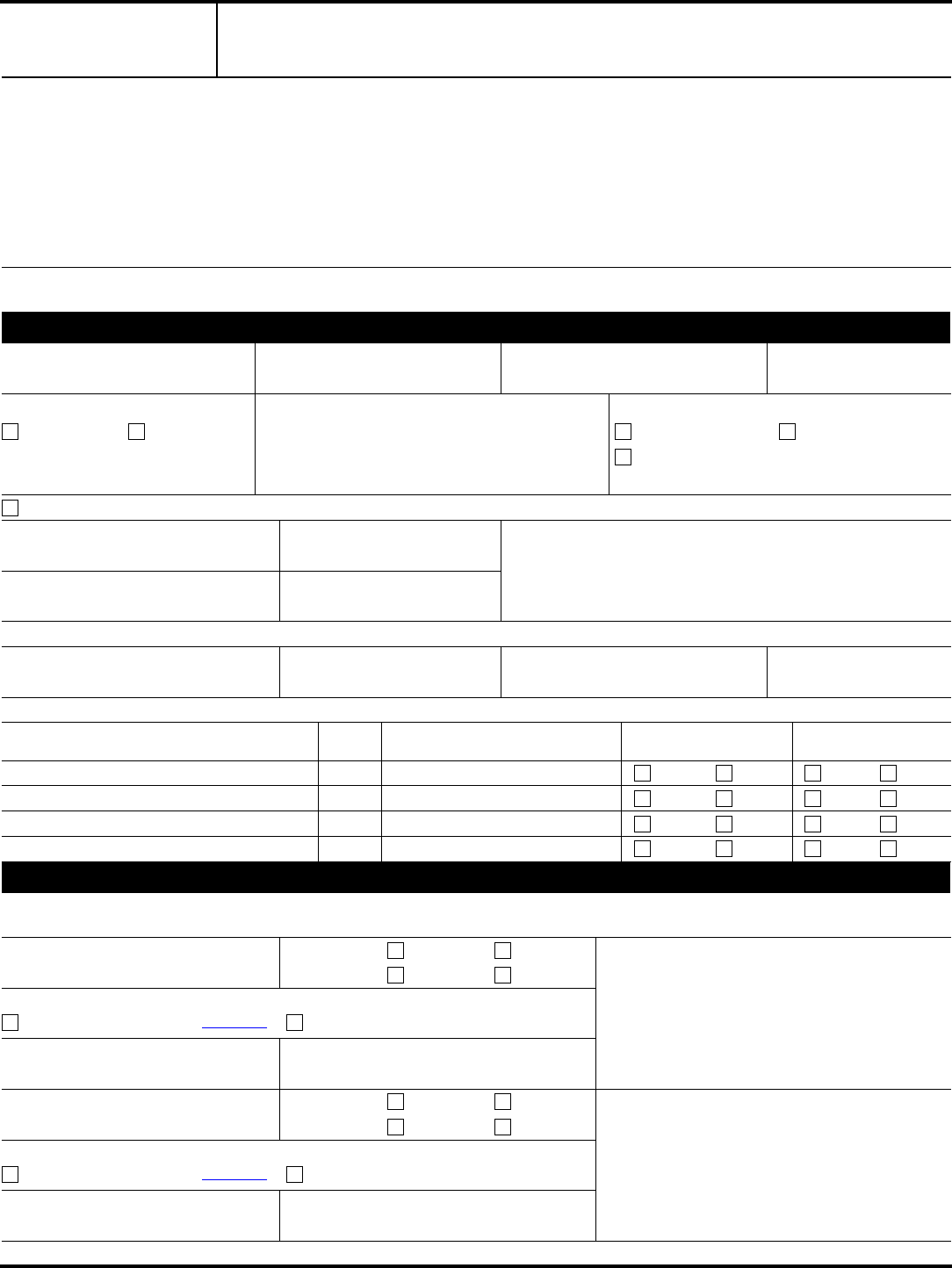

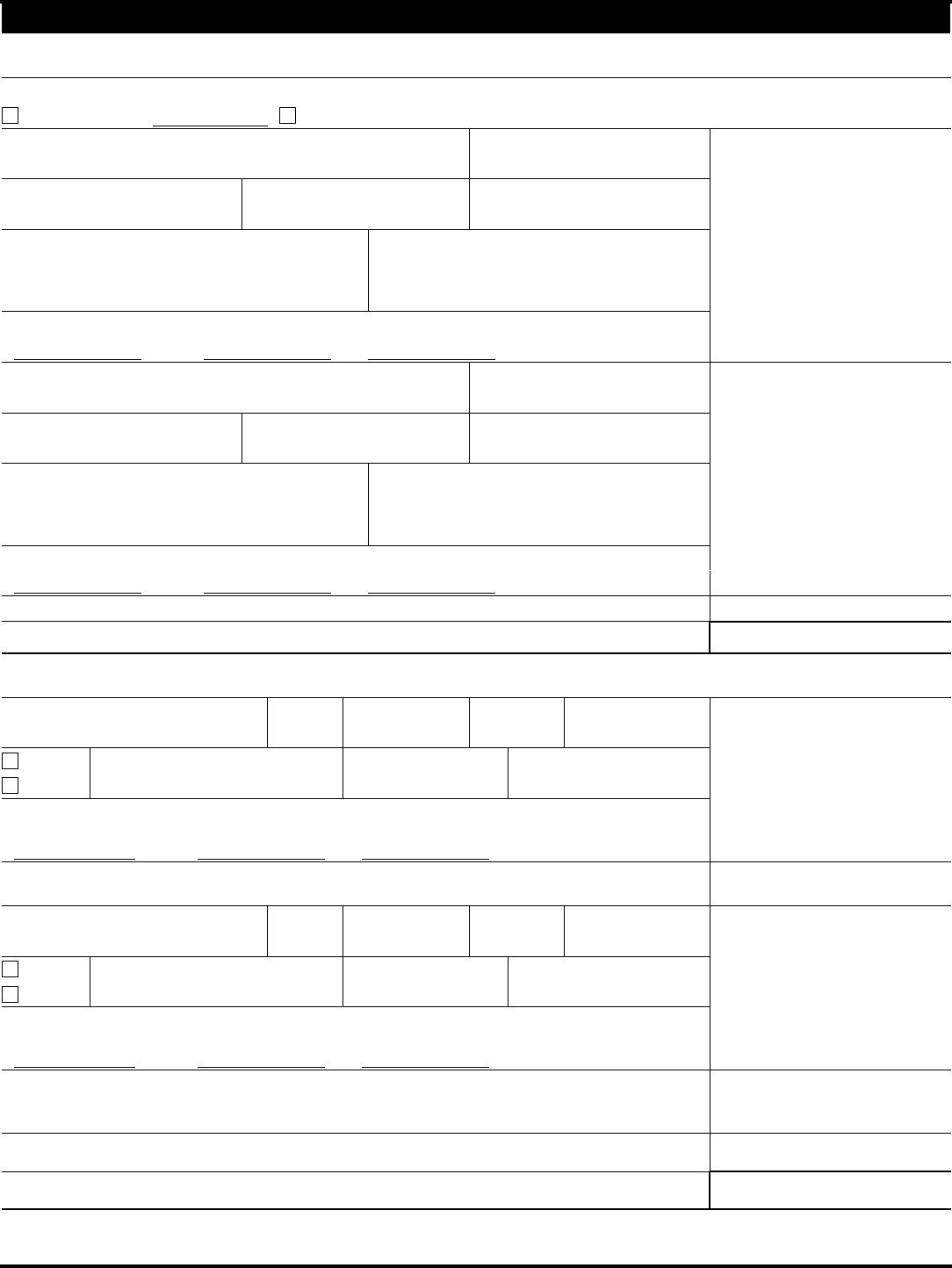

Section 1 Personal and Household Information

Last name First name

Date of birth (mm/dd/yyyy)

Social Security Number

- -

Marital status

Unmarried Married

If married, date of marriage (mm/dd/yyyy)

Home physical address (street, city, state, ZIP code)

Do you

Own your home Rent

Other (specify e.g., share rent, live with relative, etc.)

If you were married and lived in AZ, CA, ID, LA, NM, NV, TX, WA or WI within the last ten years check here

County of residence Primary phone

( ) -

Secondary phone

( ) -

FAX number

( ) -

Home mailing address (if different from above or post office box number)

Provide information about your spouse.

Spouse's last name Spouse's first name Date of birth (mm/dd/yyyy)

Provide information for all other persons in the household or claimed as a dependent.

Name Age Relationship

Claimed as a dependent

on your Form 1040

Contributes to

household income

Yes No Yes No

Yes No Yes No

Yes No Yes No

Yes No Yes No

Social Security Number

- -

Section 2 Employment Information for Wage Earners

Complete this section if you or your spouse are wage earners and receive a Form W-2. If you or your spouse have self-employment income (that is

you file a Schedule C, E, F, etc.) instead of, or in addition to wage income, you must also complete Business Information in Sections 4, 5, and 6.

Your employer’s name Pay period

Weekly Bi-weekly

Monthly Other

Employer’s address (street, city, state, ZIP code)

Do you have an ownership interest in this business

Yes (also complete and submit Form 433-B) No

Your occupation How long with this employer

(years) (months)

Spouse’s employer's name Pay period

Weekly Bi-weekly

Monthly Other

Employer’s address (street, city, state, ZIP code)

Does your spouse have an ownership interest in this business

Yes (also complete and submit Form 433-B) No

Spouse's occupation How long with this employer

(years) (months)

Catalog Number 55896Q www.irs.gov

Form

433-A (OIC) (Rev. 4-2024)

Page 2

Section 3 Personal Asset Information (Domestic and Foreign)

Use the most current statement for each type of account, such as checking, savings, money market and online accounts, stored value cards (such as a

payroll card from an employer), investment, retirement accounts (IRAs, Keogh, 401(k) plans, stocks, bonds, mutual funds, certificates of deposit) and

digital assets, or financial interests in digital assets, such as non-fungible tokens (NFTs) and virtual currencies, such as cryptocurrencies and

stablecoins, life insurance policies that have a cash value, or may be sold on a secondary market, a life settlement, and safe deposit boxes including

those located in foreign countries or jurisdictions. Asset value is subject to adjustment by IRS based on individual circumstances. Enter the total amount

available for each of the following (if additional space is needed include attachments). Ensure you also include assets located in foreign countries or

jurisdictions and add attachment(s) if additional space is needed to respond.

Round to the nearest dollar. Do not enter a negative number. If any line item is a negative number, enter "0".

Cash and Investments (domestic and foreign)

Cash Checking Savings Money Market Account/CD Online Account Stored Value Card

Bank name and country location Account number

(1a) $

Checking Savings Money Market Account/CD Online Account Stored Value Card

Bank name and country location Account number

(1b) $

Total of bank accounts from attachment (1c) $

Add lines (1a) through (1c) minus ($1,000) = (1) $

Investment account Stocks Bonds Other

Name of Financial Institution and country location Account number

Current market value

$ X .8 = $

Minus loan balance

– $

=

(2a) $

Investment account Stocks Bonds Other

Name of Financial Institution and country location Account number

Current market value

$ X .8 = $

Minus loan balance

– $

=

(2b) $

Total investment accounts from attachment. [current market value minus loan balance(s)] (2d) $

Add lines (2a) through (2d) =

(2) $

Digital asset

Description of digital asset

Number of units

Location of digital asset (exchange

account, self-hosted wallet)

Account number for assets held by

a custodian or broker

Digital asset address for self-hosted digital assets

US dollar equivalent of the digital asset as of today

$

=

(2c) $

Retirement account 401K IRA Other

Name of Financial Institution and country location Account number

Current market value

$ X .8 = $

Minus loan balance

– $

=

(3a) $

Total of retirement accounts from attachment. [current market value X .8 minus loan balance(s)] (3b) $

Add lines (3a) through (3b) = (3) $

Note: Your reduction from current market value may be greater than 20% due to potential tax consequences/withdrawal penalties.

Cash value of Life Insurance Policies

Name of Insurance Company Policy number

Current cash value

$

Minus loan balance

– $

=

(4a) $

Total cash value of life insurance policies from attachment

$

Minus loan balance(s)

– $

=

(4b) $

Add lines (4a) through (4b) = (4) $

Catalog Number 55896Q www.irs.gov

Form

433-A (OIC) (Rev. 4-2024)

Page 3

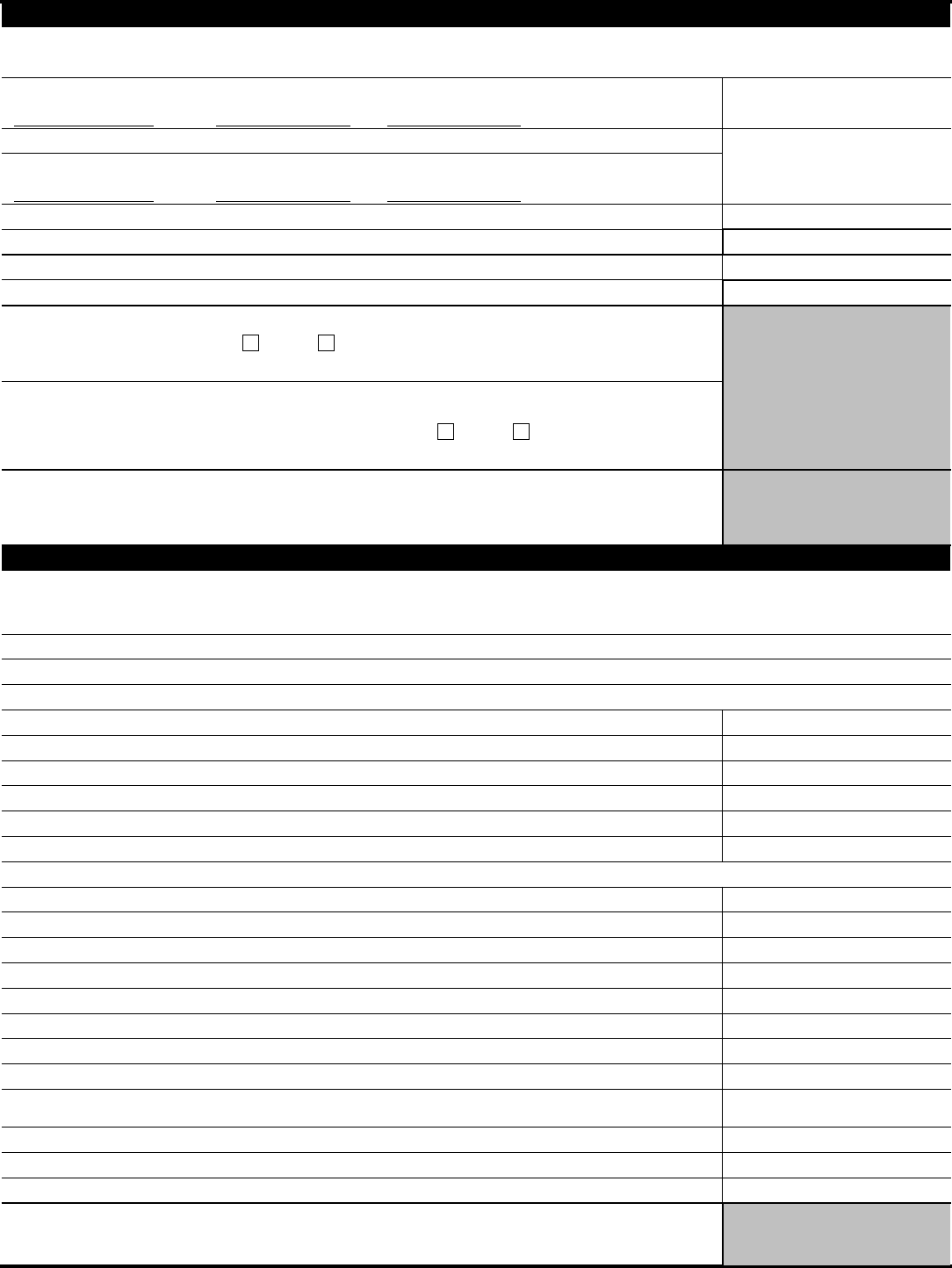

Section 3 (Continued) Personal Asset Information (Domestic and Foreign)

Real property (enter information about any house, condo, co-op, time share, etc. that you own or are buying including any assets owned by

your spouse if you live in a community property state)

Is your real property currently for sale or do you anticipate selling your real property to fund the offer amount

Yes

(listing price)

No

Property description (indicate if personal residence, rental property, vacant, etc.) Purchase date (mm/dd/yyyy)

Amount of mortgage payment Date of final payment How title is held (joint tenancy, etc.)

Location (street, city, state, ZIP code, county, and country) Lender/Contract holder name, address (street, city,

state, ZIP code)

and phone

Current market value

$ X .8 = $

Minus loan balance (mortgages, etc.)

– $

(total value of real estate) = (5a) $

Property description (indicate if personal residence, rental property, vacant, etc.) Purchase date (mm/dd/yyyy)

Amount of mortgage payment Date of final payment How title is held (joint tenancy, etc.)

Location (street, city, state, ZIP code, county, and country) Lender/Contract holder name, address (street, city,

state, ZIP code)

and phone

Current market value

$ X .8 = $

Minus loan balance (mortgages, etc.)

– $

(total value of real estate) = (5b) $

Total value of property(s) from attachment [current market value X .8 minus any loan balance(s)] (5c) $

Add lines (5a) through (5c) = (5) $

Vehicles (enter information about any cars, boats, motorcycles, etc. that you own or lease).

Include those located in foreign countries or jurisdictions. If additional space is needed, list on an attachment.

Vehicle make & model Year Date purchased Mileage License/Tag number

Lease

Own

Name of creditor Date of final payment Monthly lease/loan amount

$

Current market value

$ X .8 = $

Minus loan balance

– $

Total value of vehicle (if the vehicle

is leased, enter 0 as the total value)

=

(6a) $

Subtract $3,450 from line (6a)

(If line (6a) minus $3,450 is a negative number, enter "0")

(6b) $

Vehicle make & model Year Date purchased Mileage License/Tag number

Lease

Own

Name of creditor Date of final payment Monthly lease/loan amount

$

Current market value

$ X .8 = $

Minus loan balance

– $

Total value of vehicle (if the vehicle

is leased, enter 0 as the total value)

=

(6c) $

If you are filing a joint offer, subtract $3,450 from line (6c)

(If line (6c) minus $3,450 is a negative number, enter "0")

If you are not filing a joint offer, enter the amount from line (6c)

(6d) $

Total value of vehicles listed from attachment [current market value X .8 minus any loan balance(s)] (6e) $

Total lines (6b), (6d), and (6e) = (6) $

Catalog Number 55896Q www.irs.gov

Form

433-A (OIC) (Rev. 4-2024)

Page 4

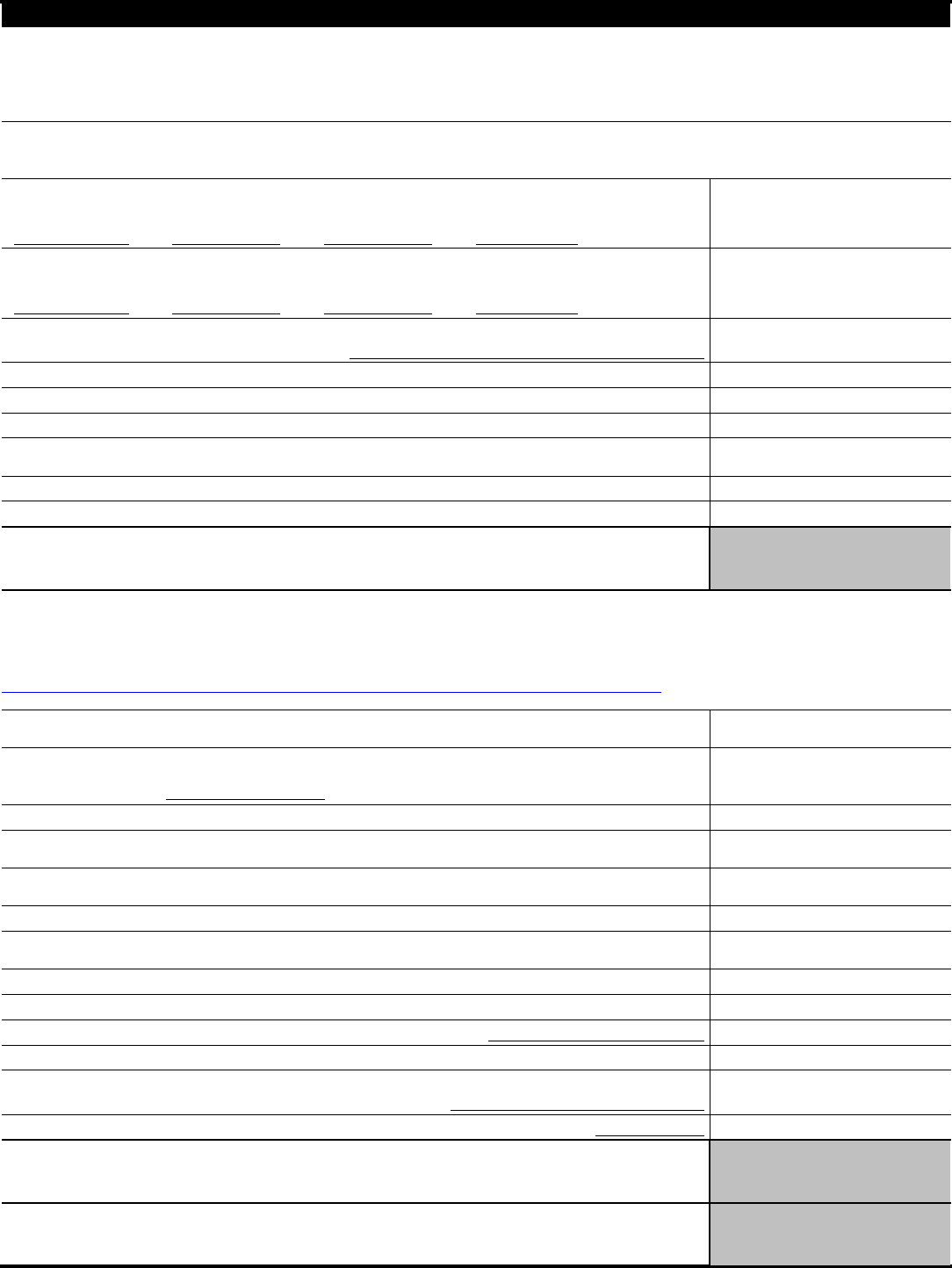

Section 3 (Continued) Personal Asset Information (Domestic and Foreign)

Other valuable items (artwork, collections, jewelry, items of value in safe deposit boxes, interest in a company or business that is not publicly traded, etc.)

Description of asset(s)

Current market value

$ X .8 = $

Minus loan balance

– $

=

(7a) $

Value of remaining furniture and personal effects (not listed above)

Description of asset

Current market value

$ X .8 = $

Minus loan balance

– $

=

(7b) $

Total value of valuable items listed from attachment [current market value X .8 minus any loan balance(s)] (7c) $

Add lines (7a) through (7c) minus IRS deduction of $11,390 =

(7) $

Do not include amount on the lines with a letter beside the number. Round to the nearest whole dollar.

Do not enter a negative number. If any line item is a negative, enter "0" on that line.

Add lines (1) through (7) and enter the amount in Box A =

Box A

Available Individual Equity in Assets

$

NOTE: If you or your spouse are self-employed, Sections 4, 5, and 6 must be completed before continuing with Sections 7 and 8.

Section 4 Self-Employed Information

If you or your spouse are self-employed (e.g., files Schedule(s) C, E, F, etc.), complete this section.

Is your business a sole proprietorship

Yes No

Name of business

Address of business (if other than personal residence)

Business telephone number

( ) -

Employer Identification Number Business website address Trade name or DBA

Description of business Total number of employees Frequency of tax deposits Average gross monthly

payroll $

Do you or your spouse have any other business interests? Include any

interest in an LLC, LLP, corporation, partnership, etc.

Yes

(percentage of ownership: )

Title

No

Business address (street, city, state, ZIP code)

Business name

Business telephone number

( ) -

Employer Identification Number

Type of business (select one)

Partnership LLC Corporation Other

Section 5 Business Asset Information (for Self-Employed) (Domestic and Foreign)

List business assets including bank accounts, digital assets (such as cryptocurrency), tools, books, machinery, equipment, business vehicles and real

property that is owned/leased/rented. If additional space is needed, attach a list of items. Do not include personal assets listed in Section 3.

Round to the nearest whole dollar. Do not enter a negative number. If any line item is a negative number, enter "0".

Cash Checking Savings Money Market Account/CD Online Account Stored Value Card

Bank name and country location Account number

(8a) $

Cash Checking Savings Money Market Account/CD Online Account Stored Value Card

Bank name and country location Account number

(8b) $

Digital asset

Description of digital asset

Number of units

Location of digital asset (exchange

account, self-hosted wallet)

Account number for assets held by

a custodian or broker

Digital asset address for self-hosted digital assets

US dollar equivalent of the digital asset as of today

$

=

(8c) $

Total bank accounts from attachment (8d) $

Add lines (8a) through (8d) = (8) $

Catalog Number 55896Q www.irs.gov

Form

433-A (OIC) (Rev. 4-2024)

Page 5

Section 5 (Continued) Business Asset Information (for Self-Employed) (Domestic and Foreign)

Description of asset

Current market value

$ X .8 = $

Minus loan balance

– $

Total value (if leased or used

in the production of income,

enter 0 as the total value)

=

(9a) $

Description of asset:

Current market value

$ X .8 = $

Minus Loan Balance

– $

Total value (if leased or used

in the production of income,

enter 0 as the total value)

=

(9b) $

Total value of assets listed from attachment [current market value X .8 minus any loan balance(s)] (9c) $

Add lines (9a) through (9c) = (9) $

IRS allowed deduction for professional books and tools of trade for individuals and sole-proprietors – (10) $

Enter the value of line (9) minus line (10). If less than zero enter zero. = (11) $

Notes Receivable

Do you have notes receivable Yes No

If yes, attach current listing that includes name(s) and amount of note(s) receivable

Accounts Receivable

Do you have accounts receivable, including e-payment, factoring

companies, and any bartering or online auction accounts

Yes No

If yes, provide a list of your current accounts receivable (include the age and amount)

Do not include amounts from the lines with a letter beside the number [for example: (9c)].

Round to the nearest whole dollar.

Do not enter a negative number. If any line item is a negative, enter "0" on that line.

Add lines (8) and (11) and enter the amount in Box B =

Box B

Available Business Equity in

Assets

$

Section 6 Business Income and Expense Information (for Self-Employed)

If you provide a current profit and loss (P&L) statement for the information below, enter the total gross monthly income on line 17 and your monthly

expenses on line 29 below. Do not complete lines (12) - (16) and (18) - (28). You may use the amounts claimed for income and expenses on your most

recent Schedule C; however, if the amount has changed significantly within the past year, a current P&L should be submitted to substantiate the claim.

Period provided beginning through

Round to the nearest whole dollar. Do not enter a negative number. If any line item is a negative number, enter "0".

Business income (you may average 6-12 months income/receipts to determine your gross monthly income/receipts)

Gross receipts (12) $

Gross rental income (13) $

Interest income (14) $

Dividends (15) $

Other income (16) $

Add lines (12) through (16) = (17) $

Business expenses (you may average 6-12 months expenses to determine your average expenses)

Materials purchased (e.g., items directly related to the production of a product or service) (18) $

Inventory purchased (e.g., goods bought for resale) (19) $

Gross wages and salaries (20) $

Rent (21) $

Supplies (items used to conduct business and used up within one year, e.g., books, office supplies, professional equipment, etc.) (22) $

Utilities/telephones (23) $

Vehicle costs (gas, oil, repairs, maintenance) (24) $

Business insurance (25) $

Current business taxes (e.g., real estate, excise, franchise, occupational, personal property, sales and employer's portion of

employment taxes)

(26) $

Secured debts (not credit cards) (27) $

Other business expenses (include a list) (28) $

Add lines (18) through (28) = (29) $

Round to the nearest whole dollar.

Do not enter a negative number. If any line item is a negative, enter "0" on that line.

Subtract line (29) from line (17) and enter the amount in Box C =

Box C

Net Business Income

$

Catalog Number 55896Q www.irs.gov

Form

433-A (OIC) (Rev. 4-2024)

Page 6

Section 7 Monthly Household Income and Expense Information

Enter your household's average gross monthly income. Gross monthly income includes wages, social security, pension, unemployment, and other

income. Examples of other income include but are not limited to: agricultural subsidies, gambling income, oil credits, rent subsidies, sharing economy

income from providing on-demand work, services or goods (e.g., Uber, Lyft, DoorDash, AirBnB, VRBO), income through digital platforms like an app or

website, etc., and recurring capital gains from the sale of securities or other property such as digital assets. Include the below information for yourself,

your spouse, and anyone else who contributes to your household’s income. This is necessary for the IRS to accurately evaluate your offer.

Monthly Household Income

Note: Entire household income should also include income that is considered not taxable and may not be included on your tax return.

Round to the nearest whole dollar.

Primary taxpayer

Gross wages

$

Social Security

+ $

Pension(s)

+ $

Other income (e.g. unemployment)

+ $

Total primary

taxpayer income

=

(30) $

Spouse

Gross wages

$

Social Security

+ $

Pension(s)

+ $

Other Income (e.g. unemployment)

+ $

Total spouse

income

=

(31) $

(32) $

Distributions (e.g., income from partnerships, sub-S Corporations, etc.) (34) $

Net rental income (35) $

Net business income from Box C [Deductions for non-cash expenses on Schedule C (e.g., depreciation, depletion, etc.) are

not permitted as an expense for offer purposes and must be added back in to the net income figure]

(36) $

Child support received (37) $

Alimony received (38) $

Round to the nearest whole dollar.

Do not enter a negative number. If any line item is a negative, enter "0" on that line.

Add lines (30) through (38) and enter the amount in Box D =

Box D

Total Household Income

$

Food, clothing, and miscellaneous (e.g., housekeeping supplies, personal care products, minimum payment on credit card).

A reasonable estimate of these expenses may be used

(39) $

Housing and utilities (e.g., rent or mortgage payment and average monthly cost of property taxes, home insurance,

maintenance, dues, fees and utilities including electricity, gas, other fuels, trash collection, water, cable television and internet,

telephone, and cell phone)

monthly rent payment

(40) $

Vehicle loan and/or lease payment(s) (41) $

Vehicle operating costs (e.g., average monthly cost of maintenance, repairs, insurance, fuel, registrations, licenses,

inspections, parking, tolls, etc.)

. A reasonable estimate of these expenses may be used

(42) $

Public transportation costs (e.g., average monthly cost of fares for mass transit such as bus, train, ferry, etc.). A reasonable

estimate of these expenses may be used (43) $

Health insurance premiums (44) $

Out-of-pocket health care costs (e.g. average monthly cost of prescription drugs, medical services, and medical supplies like

eyeglasses, hearing aids, etc.)

(45) $

Court-ordered payments (e.g., monthly cost of any alimony, child support, etc.) (46) $

Child/dependent care payments (e.g., daycare, etc.) (47) $

Life insurance premiums

Life insurance policy amount

(48) $

Current monthly taxes (e.g., monthly cost of federal, state, and local tax, personal property tax, etc.) (49) $

Interest, dividends, and royalties (33) $

Additional sources of income used to support the household, e.g., non-liable spouse, or anyone else who may

contribute to the household income, etc.

List source(s)

(50) $

Enter the amount of your monthly delinquent state and/or local tax payment(s)

. Total tax owed

(51) $

Round to the nearest whole dollar.

Do not enter a negative number. If any line item is a negative, enter "0" on that line.

Add lines (39) through (51) and enter the amount in Box E =

Secured debts/Other (e.g., any loan where you pledged an asset as collateral not previously listed, government guaranteed

student loan, employer required retirement or dues)

List debt(s)/expense(s)

Box E

Total Household Expenses

$

Round to the nearest whole dollar.

Do not enter a negative number. If any line item is a negative, enter "0" on that line.

Subtract Box E from Box D and enter the amount in Box F =

Box F

Remaining Monthly Income

$

Monthly Household Expenses

Enter your average monthly expenses.

Note: For expenses claimed in boxes (39) and (45) only, you should list the full amount of the allowable standard even if the

actual amount you pay is less. For the other boxes input your actual expenses. You may find the allowable standards at

IRS.gov/Businesses/Small-Businesses-&-Self-Employed/Collection-Financial-Standards.

Round to the nearest whole dollar.

Catalog Number 55896Q www.irs.gov

Form

433-A (OIC) (Rev. 4-2024)

Page 7

Section 8 Calculate Your Minimum Offer Amount

If you will pay your offer in 5 or fewer payments within 5 months or less, multiply "Remaining Monthly Income" (Box F) by 12 to get "Future Remaining

Income" (Box G). Do not enter a number less than $0.

Enter the total from Box F

$

X 12 =

Box G Future Remaining Income

$

If you will pay your offer in 6 to 24 months, multiply "Remaining Monthly Income" (Box F) by 24 to get "Future Remaining Income" (Box H). Do not enter

a number less than $0.

Enter the total from Box F

$

X 24 =

Box H Future Remaining Income

$

Determine your minimum offer amount by adding the total available assets from Box A and Box B (if applicable) to the amount in either Box G or Box H.

Enter the amount from Box A

plus Box B (if applicable)

$

+

Enter the amount from either

Box G or Box H

$

=

Offer Amount

Your offer must be more than zero ($0). Do

not leave blank. Use whole dollars only.

$

Place the offer amount shown above on the Form 656, Section 4, Payment Terms, unless you cannot pay that amount due to

special circumstances. If you cannot pay that amount due to special circumstances, place the amount you can pay on the

Form 656, Section 4, Payment Terms, and explain your special circumstances on the Form 656, Section 3, Reason for Offer.

Section 9 Other Information

Additional information IRS needs to consider settlement of your tax debt. If you or your business are currently in a bankruptcy proceeding,

you are not eligible to apply for an offer.

Have you filed bankruptcy in the past 7 years (if yes, answer the following)

Yes No

Date filed (mmddyyyy)

Date dismissed (mmddyyyy) Date discharged (mmddyyyy)

Petition no. Location filed

In the past 10 years, have you lived outside of the U.S. for 6 months or longer (if yes, answer the following) Yes No

Dates lived abroad: From (mmddyyyy) To (mmddyyyy)

Are you a party to or involved in litigation (if yes, answer the following) Yes No

Defendant

Plaintiff

Location of filing Docket/Case numberRepresented by

Possible completion date (mmddyyyy) Subject of litigation

$

Amount of dispute

If yes and the litigation included tax debt, provide the types of tax and periods involved

NoYesAre you or have you ever been party to any litigation involving the IRS/United States (including any tax litigation)

Are you a trustee, fiduciary, or contributor of a trust Yes No

EIN

Do you have a safe deposit box (business or personal) including those located in foreign countries or jurisdictions (if yes, answer

the following)

Yes No

Location (name, address and box number(s)) Contents

Value

$

Name of the trust

Are you the beneficiary of a trust, estate, or life insurance policy, including those located in foreign countries or jurisdictions

(if yes, answer the following)

Yes No

Place where recorded EIN

Name of the trust, estate, or policy

Anticipated amount to be received

$

When will the amount be received

The next steps calculate your minimum offer amount. The amount of time you take to pay your offer in full will affect your minimum offer amount. Paying

over a shorter period of time will result in a smaller minimum offer amount.

Note: The multipliers below (12 and 24) and the calculated offer amount (which included the amount(s) allowed for vehicles and bank

accounts) do not apply if the IRS determines you have the ability to pay your tax debt in full within the legal period to collect.

Round to the nearest whole dollar.

Catalog Number 55896Q www.irs.gov

Form

433-A (OIC) (Rev. 4-2024)

Page 8

Section 9 (Continued) Other Information

In the past 10 years, have you transferred any asset with a fair market value of more than $10,000 including real property, for

less than their full value (if yes, answer the following)

Yes No

List asset(s)

Value at time of transfer

$

Date transferred (mmddyyyy)

To whom or where was it transferred

Do you have any assets or own any real property outside the U.S. Yes No

If yes, provide description, location, and value

Do you have any funds being held in trust by a third party Yes No

If yes, how much $ Where

Section 10 Signatures

Under penalties of perjury, I declare that I have examined this offer, including accompanying documents, and to the best of my knowledge it

is true, correct, and complete.

Signature of Taxpayer

Date (mm/dd/yyyy)

Signature of Spouse

Date (mm/dd/yyyy)

Remember to include all applicable attachments listed below.

Copies of the most recent pay stub, earnings statement, etc., from each employer.

Copies of the most recent statement for each investment and retirement account.

Copies of the most recent statement, etc., from all other sources of income such as pensions, Social Security, rental income,

interest and dividends (including any received from a related partnership, corporation, LLC, LLP, etc.), court order for child

support, alimony, royalties, agricultural subsidies, gambling income, oil credits, rent subsidies, sharing economy income from

providing on-demand work, services or goods (e.g., Uber, Lyft, AirBnB, VRBO), income through digital platforms like an app or

website, etc., and recurring capital gains from the sale of securities or other property such as digital assets.

Copies of individual complete bank statements for the three most recent months. If you operate a business, copies of the six

most recent complete statements for each business bank account.

Completed Form 433-B (Collection Information Statement for Businesses) if you or your spouse have an interest in a business

entity other than a sole-proprietorship.

Copies of the most recent statement from lender(s) on loans such as mortgages, second mortgages, vehicles, etc., showing

monthly payments, loan payoffs, and balances.

List of Accounts Receivable or Notes Receivable, if applicable.

Verification of delinquent State/Local Tax Liability showing total delinquent state/local taxes and amount of monthly payments, if

applicable.

Copies of court orders for child support/alimony payments claimed in monthly expense section.

Copies of Trust documents if applicable per Section 9.

Documentation to support any special circumstances described in the “Explanation of Circumstances” on Form 656, if applicable.

Attach a Form 2848, Power of Attorney and Declaration of Representative, if you would like your attorney, CPA, or enrolled agent

to represent you and you do not have a current form on file with the IRS. Ensure all years and forms involved in your offer are

listed on Form 2848 and include the current tax year. Check the appropriate box to ensure copies of communications are sent to

your representative.

Completed and signed current Form 656.

Catalog Number 55897B www.irs.gov

Form

433-B (OIC) (Rev. 4-2024)

Form 433-B (OIC)

(April 2024)

Department of the Treasury — Internal Revenue Service

Collection Information Statement for Businesses

Complete this form if your business is a

● Corporation

● Partnership

● Limited Liability Company (LLC) classified as a corporation

● Other LLC

Note: If your business is a sole proprietorship do not use this form. Instead, complete Form 433-A (OIC) Collection Information Statement for

Wage Earners and Self-Employed Individuals. This form should only be used with the Form 656, Offer in Compromise.

Include attachments if additional space is needed to respond completely to any question.

Section 1 Business Information (Domestic and Foreign)

Business name Employer Identification Number

Business physical address (street, city, state, ZIP code)

Primary phone

( ) -

Secondary phone

( ) -

Business website address

County of business location

Description of business and DBA or "Trade Name"

Business mailing address (if different from above or post office box number)

FAX number

( ) -

Federal contractor

Yes No

Total number of employees

Check here if you are the only employee

Frequency of tax deposits Average gross monthly payroll

$

Does the business outsource its payroll processing and tax return

preparation for a fee

Yes No

If yes, list provider name and address in box below

(street, city, state, ZIP code)

Provide information about all partners, officers, LLC members, major shareholders (domestic and foreign), etc., associated with the business.

Include attachments if additional space is needed.

Last name First name Title

Percent of ownership and annual salary Social Security Number

- -

Home address (street, city, state, ZIP code)

Primary phone

( ) -

Secondary phone

( ) -

Last name First name Title

Percent of ownership and annual salary Social Security Number

- -

Home address (street, city, state, ZIP code)

Primary phone

( ) -

Secondary phone

( ) -

Last name First name Title

Percent of ownership and annual salary Social Security Number

- -

Home address (street, city, state, ZIP code)

Primary phone

( ) -

Secondary phone

( ) -

Catalog Number 55897B www.irs.gov

Form

433-B (OIC) (Rev. 4-2024)

Page 2

Section 2 Business Asset Information (Domestic and Foreign)

Gather the most current statement from banks, lenders on loans, mortgages (including second mortgages), monthly payments, loan balances, and

accountant's depreciation schedules, if applicable. Also, include make/model/year/mileage of vehicles and current value of business assets. To estimate

the current value, you may consult resources like Kelley Blue Book (www.kbb.com), NADA (www.nada.com), local real estate postings of properties similar

to yours, and any other websites or publications that show what the business assets would be worth if you were to sell them. Asset value is subject to

adjustment by IRS. Enter the total amount available for each of the following (if additional space is needed, please include attachments).

Round to the nearest dollar. Do not enter a negative number. If any line item is a negative number, enter "0".

Cash and investments (domestic and foreign)

Cash Checking Savings Money Market Account/CD Online Account Stored Value Card

Bank name and country location Account number

(1a) $

Cash Checking Savings Money Market Account/CD Online Account Stored Value Card

Bank name and country location Account number

(1b) $

Cash Checking Savings Money Market Account/CD Online Account Stored Value Card

Bank name and country location Account number

(1c) $

Total bank accounts from attachment (1d) $

Add lines (1a) through (1d) = (1) $

Investment account Stocks Bonds Other

Name of Financial Institution and country location Account number

Current market value

$ X .8 = $

Minus loan balance

– $

=

(2a) $

Investment Account: Stocks Bonds Other

Name of Financial Institution and country location Account number

Current market value

$ X .8 = $

Minus loan balance

– $

=

(2b) $

Digital asset

Description of digital asset

Number of units

Location of digital asset (exchange

account, self-hosted wallet)

Account number for assets held by

a custodian or broker

Digital asset address for self-hosted digital assets

US dollar equivalent of the digital asset as of today

$

=

(2c) $

Total investment accounts from attachment. [current market value minus loan balance(s)] (2d) $

Add lines (2a) through (2d) = (2) $

Notes Receivable

Do you have notes receivable Yes No

If yes, attach current listing which includes name, age, and amount of note(s) receivable

Accounts Receivable

Do you have accounts receivable, including e-payment, factoring

companies, and any bartering or online auction accounts

Yes No

If yes, provide a list of name, age, and amount of the current accounts receivable

Catalog Number 55897B www.irs.gov

Form

433-B (OIC) (Rev. 4-2024)

Page 3

Section 2 (Continued) Business Asset Information (Domestic and Foreign)

If the business owns more properties, vehicles, or equipment than shown in this form, please list on a separate attachment.

Real estate (buildings, lots, commercial property, etc.)

Is your real property currently for sale or do you anticipate selling your real property to fund the offer amount

Yes

(listing price)

No

Property address (street address, city,

state, ZIP code, county, and country)

Property description (indicate if rental property, vacant, etc.) Date purchased

Monthly mortgage payment Date of final payment

Name of lender/contract holder

Current market value

$ X .8 = $

Minus loan balance (mortgages, etc.)

– $

Total value of real estate =

(3a) $

Property address (street address, city,

state, ZIP code, county, and country)

Property description (indicate if rental property, vacant, etc.) Date purchased

Monthly mortgage payment Date of final payment

Name of lender/contract holder

Current market value

$ X .8 = $

Minus loan balance (mortgages, etc.)

– $

Total value of real estate =

(3b) $

Total value of property(s) listed from attachment [current market value X .8 minus any loan balance(s)] (3c) $

Add lines (3a) through (3c) = (3) $

Business vehicles (cars, boats, motorcycles, trailers, etc.). Include those located in foreign countries or jurisdictions. If additional space is needed, list on an

attachment.

Vehicle make & model Year Date purchased Mileage or use hours License/Tag number

Lease

Own

Name of creditor Date of final payment Monthly lease/loan amount

$

Current market value

$ X .8 = $

Minus loan balance

– $

Total value of vehicle (if the vehicle

is leased, enter 0 as the total value)

=

(4a) $

Mileage or use hours License/Tag numberVehicle make & model Year Date purchased

Lease

Own

Name of creditor Date of final payment Monthly lease/loan amount

$

Current market value

$ X .8 = $

Minus loan balance

– $

Total value of vehicle (if the vehicle

is leased, enter 0 as the total value)

=

(4b) $

Vehicle make & model Year Date purchased Mileage or use hours License/Tag number

Lease

Own

Name of creditor Date of final payment Monthly lease/loan amount

$

Current market value

$ X .8 = $

Minus loan balance

– $

Total value of vehicle (if the vehicle

is leased, enter 0 as the total value)

=

(4c) $

Total value of vehicles listed from attachment [current market value X .8 minus any loan balance(s)] (4d) $

Add lines (4a) through (4d) = (4) $

Catalog Number 55897B www.irs.gov

Form

433-B (OIC) (Rev. 4-2024)

Page 4

Section 2 (Continued) Business Asset Information (Domestic and Foreign)

Other business equipment

[If you have more than one piece of equipment, please list on a separate attachment and put the total of all equipment in box (5b)]

Type of equipment

Current market value

$ X .8 = $

Minus loan balance

– $

Total value of equipment

(if leased or used in the production of

income enter 0 as the total value)

=

(5a) $

Total value of equipment listed from attachment [current market value X .8 minus any loan balance(s)] (5b) $

Total value of all business equipment

Add lines (5a) and (5b) =

(5) $

Do not include amount on the lines with a letter beside the number. Round to the nearest dollar.

Do not enter a negative number. If any line item is a negative number, enter "0" on that line.

Add lines (1) through (5) and enter the amount in Box A =

Box A

Available Equity in Assets

$

Section 3 Business Income Information

Enter the average gross monthly income of your business. To determine your gross monthly income use the most recent 6-12 months documentation of

commissions, invoices, gross receipts from sales/services, etc.; most recent 6-12 months earnings statements, etc., from every other source of income (such as

rental income, interest and dividends, or subsidies); or you may use the most recent 6-12 months Profit and Loss (P&L) to provide the information of income and

expenses.

Note: If you provide a current profit and loss statement for the information below, enter the total gross monthly income in Box B below. Do not

complete lines (6) - (10).

Period provided beginning through

Gross receipts (6) $

Gross rental income (7) $

Interest income (8) $

Dividends (9) $

Other income (specify on attachment)

(10) $

Round to the nearest dollar.

Do not enter a negative number. If any line item is a negative number, enter "0" on that line.

Add lines (6) through (10) and enter the amount in Box B =

Box B

Total Business Income

$

Section 4 Business Expense Information

Enter the average gross monthly expenses for your business using your most recent 6-12 months statements, bills, receipts, or other documents

showing monthly recurring expenses. Deductions for non-cash expenses (e.g., depreciation, depletion, etc.) are not permitted as an expense for

offer purposes.

Note: If you provide a current profit and loss statement for the information below, enter the total monthly expenses in Box C below. Do not

complete lines (11) - (20).

Period provided beginning through

Materials purchased (e.g., items directly related to the production of a product or service)

(11) $

Inventory purchased (e.g., goods bought for resale)

(12) $

Gross wages and salaries (13) $

Rent (14) $

Supplies (items used to conduct business and used up within one year, e.g., books, office supplies, professional

equipment, etc.)

(15) $

Utilities/telephones (16) $

Vehicle costs (gas, oil, repairs, maintenance)

(17) $

Insurance (other than life)

(18) $

Current taxes (e.g., real estate, state, and local income tax, excise franchise, occupational, personal property,

sales and employer's portion of employment taxes, etc.)

(19) $

Other expenses (e.g., secured debt payments. Specify on attachment. Do not include credit card payments)

(20) $

Round to the nearest dollar.

Do not enter a negative number. If any line item is a negative number, enter "0" on that line.

Add lines (11) through (20) and enter the amount in Box C =

Round to the nearest dollar.

Do not enter a negative number. If any line item is a negative number, enter "0" on that line.

Subtract Box C from Box B and enter the amount in Box D =

Box C

Total Business Expenses

$

Box D

Remaining Monthly Income

$

Catalog Number 55897B www.irs.gov

Form

433-B (OIC) (Rev. 4-2024)

Page 5

Section 5

Calculate Your Minimum Offer Amount

The next steps calculate your minimum offer amount. The amount of time you take to pay your offer in full will affect your minimum offer amount. Paying

over a shorter period of time will result in a smaller minimum offer amount.

Note: The multipliers below (12 and 24) and the calculated offer amount do not apply if IRS determines you have the ability to pay your tax

debt in full within the legal period to collect.

Round to the nearest whole dollar.

If you will pay your offer in 5 or fewer payments within 5 months or less, multiply "Remaining Monthly Income" (Box D) by 12 to get "Future Remaining

Income." Do not enter a number less than zero.

Enter the total from Box D

$

X 12 =

Box E Future Remaining Income

$

If you will pay your offer in 6 to 24 months, multiply "Remaining Monthly Income" (Box D) by 24 to get "Future Remaining Income". Do not enter a

number less than zero.

Enter the total from Box D

$

X 24 =

Box F Future Remaining Income

$

Determine your minimum offer amount by adding the total available assets from Box A to the amount in either Box E or Box F. Your offer amount must

be more than zero.

Enter the amount from Box A*

$

+

Enter the amount from either

Box E or Box F

$

=

Offer Amount

Your offer must be more than zero ($0).

Do not leave blank. Use whole dollars only.

Place your offer amount on Form 656

Section 4, Payment Terms.

$

*You may exclude any equity in income producing assets (except real estate) shown in Section 2 of this form.

Section 6 Other Information

Additional information IRS needs to consider settlement of your tax debt. If this business is currently in a bankruptcy proceeding, the

business is not eligible to apply for an offer.

Is the business currently in bankruptcy

Yes No

Has the business filed bankruptcy in the past 10 years

Yes No

If yes, provide

Date filed (mm/dd/yyyy)

Date dismissed or discharged (mm/dd/yyyy)

Petition no. Location filed

Does this business have other business affiliations (e.g., subsidiary or parent companies)

Yes No

If yes, list the name and Employer Identification Number

Do any related parties (e.g., partners, officers, employees) owe money to the business

Yes No

Is the business currently, or in the past, party to litigation

If yes, answer the following

Yes No

If yes and the litigation included tax debt, provide the types of tax and periods involved.

NoYes

Are you or have you been party to litigation involving the IRS/United States (including any tax litigation)

Defendant

Plaintiff

Location of filing Docket/Case numberRepresented by

Possible completion date (mmddyyyy) Subject of litigation

$

Amount in dispute

Catalog Number 55897B www.irs.gov

Form

433-B (OIC) (Rev. 4-2024)

Page 6

Section 7 Signatures

Under penalties of perjury, I declare that I have examined this offer, including accompanying documents, and to the best of my knowledge it

is true, correct, and complete.

Signature of Taxpayer Title Date (mm/dd/yyyy)

Remember to include all applicable attachments from the list below.

A current Profit and Loss statement covering at least the most recent 6–12 month period, if appropriate.

Copies of the six most recent complete bank statements for each business account and copies of the three most recent

statements for each investment account.

If an asset is used as collateral on a loan, include copies of the most recent statement from lender(s) on loans, monthly

payments, loan payoffs, and balances.

Copies of the most recent statement of outstanding accounts and notes receivable.

Copies of the most recent statements from lenders on loans, mortgages (including second mortgages), monthly payments, loan

payoffs, and balances.

Copies of relevant supporting documentation of special circumstances described in the Section 3 on Form 656, if applicable.

Attach a Form 2848, Power of Attorney and Declaration of Representative, if you would like your attorney, CPA, or enrolled

agent to represent you and you do not have a current form on file with the IRS. Ensure all years and forms involved in your offer

are listed on Form 2848 and include the current tax year. Check the appropriate box to ensure copies of communications are

sent to your representative.

Completed and current signed Form 656.

In the past 3 years have you transferred any real property (land, house, etc.)

Yes No

If yes, list the type of property, value, and date of the transfer

Has the business been located outside the U.S. for 6 months or longer in the past 10 years

Yes No

Does the business have any funds being held in trust by a third party

Yes No

If yes, how much $ Where

Yes No

Does the business have any lines of credit

If yes, credit limit $ Amount owed $

What property secures the line of credit

Do you have any assets or own any real property outside the U.S.

Yes No

If yes, please provide description, location, and value

In the past 10 years, has the business transferred any asset with a fair market value of more than $10,000, including real property, for less than its full

value

Yes No

If yes, provide date, value, and type of asset transferred

Other Information Section 6 (Continued)

Catalog Number 16728N www.irs.gov

Form

656 (Rev. 4-2024)

Form 656

(April 2024)

Offer in Compromise

Department of the Treasury — Internal Revenue Service

To: Commissioner of Internal Revenue Service

In the following agreement, the pronoun "we" may be assumed in place of "I" when there are joint liabilities and both

parties are signing this agreement.

I submit this offer to compromise the tax liabilities plus any interest, penalties, additions to tax, and additional amounts

required by law for the tax type and period(s) marked in Section 1 or Section 2 below.

IRS Received Date

(COIC use only)

Did you use the Pre-Qualifier tool prior to filling out this form? Locate the tool on our website at IRS.gov/OICtool

or by scanning the QR code on your smart device.

Yes No

Note: The use of the Pre-Qualifier tool is not mandatory before sending in your offer. However, it is recommended.

Attention: You must submit separate offers if either spouse has separate tax liabilities.

Include the $205 fee and initial payment with your Form 656 unless you qualify for the Low-Income Certification. Fill out

either Section 1 or Section 2, but not both.

If you are a 1040, U.S. Individual Income Tax Return, filer, an individual with personal liability for Excise tax, individual responsible for Trust Fund

Recovery Penalty, self-employed individual, or individual personally responsible for partnership liabilities, you should fill out Section 1.

Section 1 Individual Information (Form 1040 filers)

Your first name, middle initial, last name Social Security Number (SSN), Individual Taxpayer or Identification

Number (ITIN) (if applicable)

- -

If a joint offer, spouse's first name, middle initial, last name Social Security Number (SSN), Individual Taxpayer or Identification

Number (ITIN) (if applicable)

- -

Your home physical address (street, city, state, ZIP code, county of residence)

Your home mailing address (if different from above or post office box number)

Is this a new address since your last filed tax return

Yes No

If yes, would you like us to update our records to this address

Yes No

Your Employer Identification Number (if applicable)

-

Individual Tax Periods (For Individual or Sole-Proprietor Tax Debt Only) List all years/periods owed

Form 1040 U.S. Individual Income Tax Return [e.g., 12-31-2018]

Trust Fund Recovery Penalty as a responsible person of (enter business name)

for failure to pay withholding and Federal Insurance Contributions Act taxes (Social Security taxes), for period(s) ending [e.g., 03-31-2019]

Form 941 Employer's Quarterly Federal Tax Return - Quarterly period(s)

Form 940 Employer's Annual Federal Unemployment (FUTA) Tax Return - Year(s) [e.g., 12-31-2018]

Other Federal Tax(es) [specify type(s) and period(s)]

Note: If you need more space, use attachment and title it “Attachment to Form 656 dated .” Make sure to sign and date the

attachment.

Warning: The IRS will not compromise any amounts of restitution assessed by the IRS. Any liability arising from restitution is excluded from this offer.

Also, the IRS will not compromise any liability for which an election under IRC § 965(i) is made; such liabilities are excluded from this offer. Any offer

containing a liability for which payment is being deferred under IRC § 965(h)(1) can only be processed for investigation if an acceleration of payment

under section 965(h)(3) and the regulations thereunder has occurred and no portion of the liability to be compromised resulted from entering into a

transfer agreement under section 965(h)(3).

Catalog Number 16728N www.irs.gov

Form

656 (Rev. 4-2024)

Page 2

Low-Income Certification (Individuals and Sole Proprietors Only)

Do you qualify for Low-Income Certification? You qualify if your adjusted gross income, as determined by your most recently filed Individual Income Tax

return (Form 1040) or your household’s gross monthly income from Form 433-A(OIC) x 12, is equal to or less than the amount shown in the chart below

based on your family size and where you live. If you qualify, you are not required to submit any payments or the application fee upon submission or

during the consideration of your offer. If your business is other than a sole proprietor or the offer is being filed for a deceased individual, you do not

qualify for Low-Income Certification. The IRS will verify whether you qualify for Low-Income Certification.

Note: By checking one of the boxes below you are certifying that your adjusted gross income or your household’s gross monthly income x 12

and size of your family qualify you for the Low-Income Certification.

I qualify for the Low-Income Certification because my adjusted gross income for my household's size is equal to or less than the amount shown in

the table below.

I qualify for the Low-Income Certification because my household's size and gross monthly income x 12 is equal to or less than the income shown in

the table below.

Size of family unit 48 contiguous states, D.C., and U.S. Territories Alaska Hawaii

1 $36,450 $45,525 $41,925

2 $49,300 $61,600 $56,700

3 $62,150 $77,675 $71,475

4 $75,000 $93,750 $86,250

5 $87,850 $109,825 $101,025

6 $100,700 $125,900 $115,800

7 $113,550 $141,975 $130,575

8 $126,400 $158,050 $145,350

For each additional person, add $12,850 $16,075 $14,775

Business Information (Form 1120, 1065, etc., filers)

Business Tax Periods (If Your Offer is for Business Tax Debt Only) List all years/periods owed

Form 1120 U.S. Corporate Income Tax Return - [e.g., 12-31-2019]

Form 941 Employer's Quarterly Federal Tax Return - [e.g., 03-31-2019]

Form 940 Employer's Annual Federal Unemployment (FUTA) Tax Return - [e.g., 12-31-2018]

Other Federal Tax(es) [specify type(s) and period(s)]

Note: If you need more space, use attachment and title it “Attachment to Form 656 dated .” Make sure to sign and date the

attachment.

Section 2

If your business is a Corporation, Partnership, LLC, or LLP and you want to compromise those tax debts, you must complete this section. You must also

include all required documentation including the Form 433-B (OIC), a $205 application fee, and initial payment.

Business name

Business physical address (street, city, state, ZIP code)

Business mailing address (street, city, state, ZIP code)

Employer Identification Number

(EIN)

-

Name and title of primary contact Telephone number

( ) -

IF YOU QUALIFY FOR THE LOW-INCOME CERTIFICATION DO NOT INCLUDE ANY PAYMENTS WITH YOUR OFFER. Generally these payments